The Bruges Group spearheaded the intellectual battle to win a vote to leave the European Union and, above all, against the emergence of a centralised EU state.

Bruges Group Blog

The German Federal Audit Office ('Bundesrechnungshof') has warned that the Bundesbank may need a bailout due to losses on the EUR650 billion of bonds it bought as part of the Eurozone's equivalent of Quantitative Easing. The Daily Telegraph reported on this on 26 June. Of course the risk is not for the entire EUR650 billion but for the fraction by ...

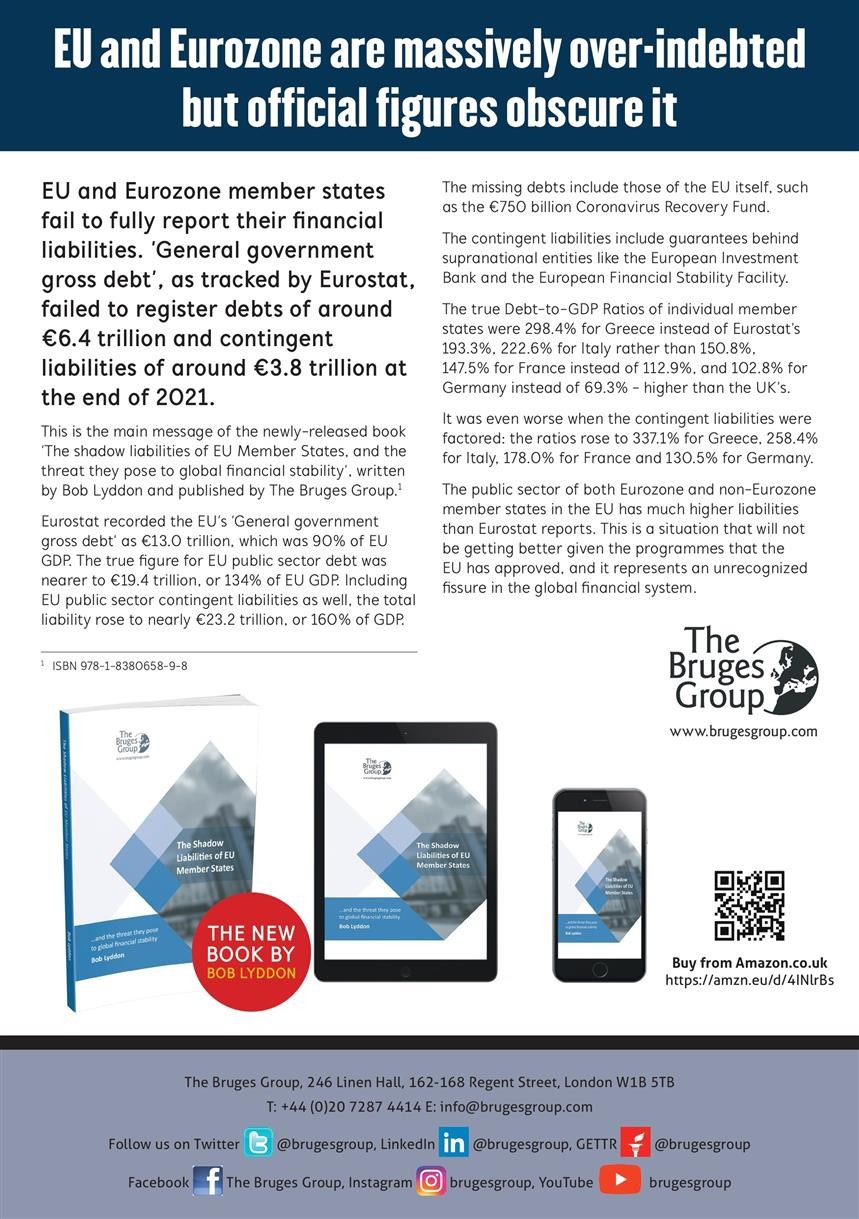

The totality of the public sector liabilities of EU and Eurozone member states is clouded in obscurity. The key measure tracked by Eurostat - 'General government gross debt' – is circumvented to such an extent that, based on year-end 2021 figures, debts of around €6.4 trillion failed to be registered, and contingent liabilities of around €3.8 trill...

The EU member states contain numerous public sector entities with borrowing powers, and whose debts fall outside the definition of member state debt as reported by Eurostat. The responsibility for the debts tracks back, one way or another, to the member state but the amounts involved are opaque. All that can be said with complete certainty is that ...

TARGET2 harbours risks even greater than the enormous ones acknowledged by the European Central Bank

There has been long and ongoing debate about the nature of the sizable loans and deposits that the Eurozone national central banks (NCBs) run with one another within the TARGET2 payment system. The debate has overlooked that the balances are nearly double what the European Central Bank (ECB) reports, and that the report only shows the amounts at th...

The programmes of the European Central Bank (ECB) are extensive, and involve greater risks than the ECB can bear, it being very thinly capitalised. Even modest losses on its programmes would require it to be recapitalised by its Eurozone shareholders – the national central banks (NCBs) of the Eurozone member states. This is laid out in the newly-re...

Net Zero is proving to be a good cover story for the European Investment Bank Group to create huge financial liabilities for the EU taxpayer. The amount looks set to exceed €1.2 trillion by the end of the current EU budget period in 2027. This is laid out in the newly-released book 'The shadow liabilities of EU Member States, and the threat they po...

The structures of the EU and Eurozone have allowed the creation of a series of supranational entities that have taken on debts whilst having little financial strength of their own: their creditworthiness depends on guarantees or capital calls from member states, without the extent of the member states' liabilities being transparent and being added ...

The public credit ratings of EU/Eurozone member states are inflated, because the credit rating agencies have not factored in the significant shadow debts and other financial liabilities bearing down on the respective member state's debt service capacity. Total financial liabilities are much higher than these agencies appear to recognise. This is th...

Global debt markets appear comfortable to absorb all of the bonds issued by the European Union for its €750 billion Coronavirus Recovery Fund on the basis that 'it all tracks back onto Germany'. This is true: the guarantee structure behind the EU's debts makes each member state liable for the entirety of them. The same debt markets do not seem to h...

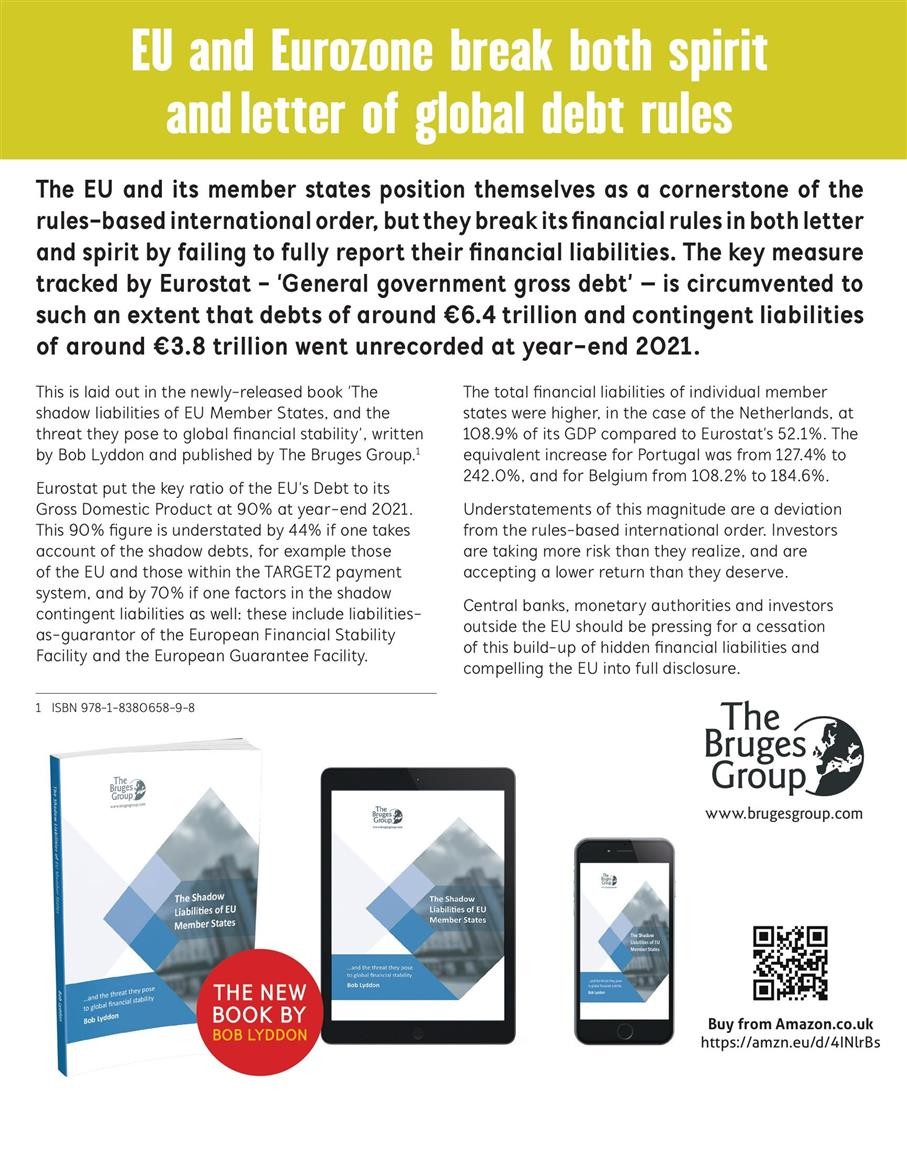

The EU and its member states position themselves as a cornerstone of the rules-based international order, but they break its financial rules in both letter and spirit by failing to fully report their financial liabilities. The key measure tracked by Eurostat - 'General government gross debt' – is circumvented to such an extent that, based on year-e...

EU and Eurozone member states fail to fully report their financial liabilities. The key measure tracked by Eurostat - 'General government gross debt' – is circumvented to such an extent that, based on year-end 2021 figures, debts of around €6.4 trillion failed to be registered, and contingent liabilities of around €3.8 trillion. This discrepancy is...

EU and Eurozone member states fail to fully report their financial liabilities. The key measure tracked by Eurostat - 'General government gross debt' – is circumvented to such an extent that, based on year-end 2021 figures, debts of around €6.4 trillion failed to be registered, and contingent liabilities of around €3.8 trillion. This discrepa...

BUY THIS BOOK &...

Anthony Coughlan is known to most of us for his heroic work for the National Platform of Ireland, which campaigns for Ireland's independence from the EU. As Michael Quinn writes, "He has tirelessly campaigned against the centralising and unaccountable EU bureaucracy; articulating instead the alternative case for a Europe of independent and co-opera...

Marathon talks have concluded between EU leaders as they battled over the details of its multibillion-euro pandemic recovery fund. With France and Germany head-to-head against the frugal four of Austria, Denmark, the Netherlands and Sweden over grants, veto rights and funding criteria, you could be mistaken for seeing the talks as the break-up of t...

The absence of a pan-European fiscal union combined with the departure of the United Kingdom have left European finances is disarray. This has been exacerbated by a crisis that has sown divisions in a frail union with poorer states demanding that richer countries foot the bill to save the Union. When Germany's constitutional court questioned t...

Almost four years after we voted to leave the European Union (EU), Boris Johnson delivered on his promise to 'GET BREXIT DONE'. Little did we know at the time (on 31st January 2020) that the year was going to bring its own woes, which are now threatening to bring down the European dream of unity, solidarity, and borderless territory. In addition to...