Any sort of trade deal with the EU is bound to result in economic meltdown. Here's how and why.

Author: John Poynton

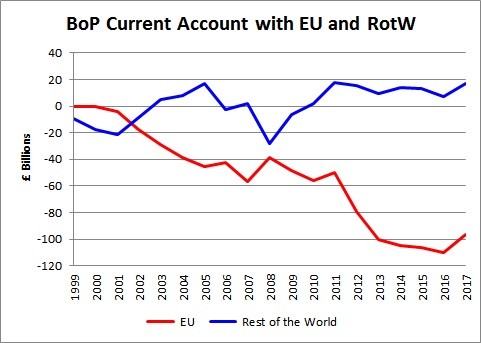

| | This graph shows our Balance of Payments Current Account – in effect our national profit and loss account, comprising mainly but not exclusively of trade – split into two separate components; our trade with the EU (the red line) and our trade with the Rest of the World ('RotW' - blue line). At the millennium our deficit with the EU was £4bn, whereas by the time of the referendum it had plummeted to £109bn, whereas our trade with the Rest of the World has moved from a loss of £17bn to a profit last year of £20bn. I have downloaded the series from the ONS website, subtracting the EU from the total to get the RotW |

At least four questions immediately arise:

It clearly isn't anything to do with exchange rates as they affect both lines. Indeed our success with the RotW would indicate that our exchange rate is correctly valued. If you are minded not to believe it has anything to do with free trade – the absence of import tariffs – then by elimination it can only be due to non-tariff regulations. That must mean that, over the past twenty years Brussels has, either surreptitiously or unwittingly, been stacking up a great mountain of such barriers which somehow and mysteriously, presumably due to the way they have been chosen, adversely affect our exports while not impeding theirs. I have no evidence for this other than by judging by results.

So does Free Trade within the Single Market have anything to do with it? (Gasp – sacrilege!)

The first thing to observe is that THERE IS NO SUCH THING AS FREE TRADE!Import tariffs are a form of taxation so, other things being equal, if you reduce them you have to increase something else, such as income tax or VAT. All you are doing is passing the buck sideways. There is nothing 'free' about it. Furthermore if you spend more of your money on imports because free trade makes them relatively cheaper, you spend less on British stuff, thereby putting workers out of a job.

Champions of Free Trade will quote the classical economists Adam Smith and David Riccardo, both of whom waxed lyrical about specialisation and division of labour, and point to modern research showing a continued global correlation between free trade and economic growth. In those days Britain was the manufacturing centre of the world, and the rest provided us with the natural resources the industrial revolution required; specialisation indeed, all protected by the Royal Navy and the Gold Standard. Everyone benefited.The role of the Gold Standard should not be overlooked. It meant that there was just one international currency, precious metals; so, if one nation developed a trade deficit its money supply would be reduced. That meant that prices and wages would also go down until its exports became competitive once more, thereby redressing the balance. It was an inherently stable system.

Today we no longer have such a system. We have multiple currencies and instability, as witnessed by the massive trade imbalances that have developed since the start of globalisation – and our joining the Single Market. Nor is there any discernible evidence of economic growth in this country as a result – witness the growing productivity gap. These imbalances produce a massive transfer of wealth from deficit countries to surplus countries, so even if a deficit country does experience some economic growth the benefit is outweighed by the loss, which makes us poorer. No wonder we are now 21st in the list by standard of living. By contrast countries such as China and Singapore, who are often held up as examples of the benefits of Free Trade, are surplus countries with a high propensity to save. Of course they now want to cash in their chips and spend them on lower import tariffs. Whereas we have record levels of personal and national debt, have accumulated losses, and thus have no chips to cash in.

I think the conclusion to be drawn from all this is that Free Trade deals are fine between countries whose trade is in balance. If trade is not in balance then a Free Trade deal will only magnify that imbalance. This is just simple mathematics. If you increase volumes of trade by equal percentages on top of a deficit then the deficit will increase in proportion, and vice versa.

So what is my conclusion about the Divergence? It is probably due to a bit of both factors – an underlying and continuing imposition of regulations, magnified by the destabilising effect of Free Trade within the Single Market.

So does a trade deficit with the EU matter?

Well of course it matters, for the simple reason it has to be financed somehow. This must be addressed at two levels - foreign currency and domestic consumer demand.

Fortunately we have a strong Capital Account surplus, so there is plenty of foreign currency around to pay for our excess imports. But hang on a sec. That money is not ours. It can be withdrawn again at any moment by those who sent it here. We are robbing Peter to pay Paul, and if Peter cottons on he is likely to panic and withdraw his funds. Then we really would be buggered. But fortunately all seems well in the short term, which is all our politicians are concerned about.

No, it is the effect on domestic demand that is the immediate problem. Other things being equal you would expect unemployment to be shooting through the roof at this point, so how come it has not?

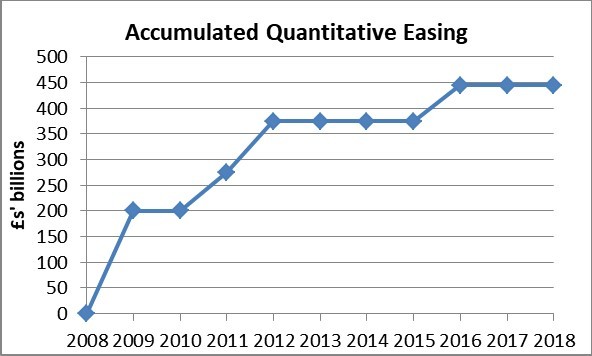

| Here is another graph (see below). It shows the accumulation of Quantitative Easing over the past ten years since the banking crisis. Popularly known as printing money it in fact involves the Bank buying illiquid assets such as gilts and corporate bonds in exchange for liquid cash. These assets accumulate in its balance sheet, and also I hope provide a good return! But if QE were used other than to offset a fall in the money supply, such as all the debts written off by the banks, then it would be highly inflationary. Thus, as the graph shows, it was stopped in 2012 after the banks had been fixed. | |

But what's this? It has been restarted again in 2016, when a further £70bn was authorised. The only possible explanation is that the Government were forced to do this to fund the losses incurred on current account. QE is not good news. It works by reducing interest rates, thereby reducing savings, which in turn reduces investment and economic growth – hence the productivity gap which, yes, started in 2008 when QE started. But more immediately it encourages people to borrow, thereby increasing consumer demand to offset the loss from the trade deficit. But as Mervyn King put it so succinctly in his recent book, The End of Alchemy, when people borrow money they are spending tomorrow's income today. The problem is that, sooner or later, tomorrow becomes today, and when that happens they not only cannot borrow any more but also have to start repaying what they borrowed yesterday. Even at very low interest rates there is a limit to how much people can borrow. And when that happens the whole edifice will come crashing down. Not only will unemployment go through the roof, but also thousands upon thousands of Brits will go bankrupt.

So what can we do about it?

Well obviously we have to take back our trade; to reduce and eliminate our deficit with the EU. That is the first domino in the line. No deal can achieve that. It would have to be a one-sided deal, and that is as likely as a free lunch. Only a No-Deal Brexit will give us the opportunity to change course and avoid the massive iceberg dead ahead. Even then it is only an opportunity, and several years of hard graft will be required forensically to identify all the non-tariff barriers that have been constructed against us and find ways of neutralising them. We shall have to give as good as we have received. This is about survival. We are in a trade war. It has been going on for twenty years and our dozy Treasury mandarins, away with the fairies in their Remainian dreamworld, have not lifted a finger to advise ministers to take action. Pacifists do not win wars.

At least a No-Deal Brexit will give us an initial boost. By raising tariffs on both sides of the Channel, volumes will be reduced. This in turn will make a start in reducing the deficit, since everything will reduce in proportion. More jobs will be created from import substitution than will be lost to export substitution - Labour Party please note!

Last but not least there will be another £22bn for the Brexit Dividend from import tariff revenues. Funny how the BBC never mentions this! 60% of our trade is with the RotW on which EU tariffs are paid right now, amounting to approx. £15bn a year. 80% of that, £12bn, is paid across to Brussels, but after a No-Deal Brexit it will stay in London. At no inflationary cost whatsoever! The remaining 40% with the EU will attract the same tariffs, assuming we put in place a mirror image of the EU tariffs, giving us a further £10bn. Inflationary? Well not very. Average tariffs are just under 5%, and our total foreign trade is about a third of our economy, so multiplied out that gives inflation of 0.667% - on a once off basis. Its peanuts.

We do not want or need anything from the EU. So why are we negotiating at all?

WE MUST TAKE BACK CONTROL OF OUR TRADE. ONLY A NO-DEAL BREXIT CAN ACHIEVE THAT.

Published and promoted by John Poynton FCA, jepoynton.com,